It’s been two weeks since the armies of Asia’s two largest economies, China and India, clashed in the Galwan Valley region of eastern Ladakh, a disputed Himalayan border area. Even as the top military commanders of Indian and Chinese armies attempt to ease tension along the Line of Actual Control (LAC), the ripple effect of the situation is being felt across the two countries.

Noticeably, the standoff has given air to the public discontent against Chinese firms operating in India as well as Indian companies that have received money from China.

Earlier this week, several delivery executives of Indian food tech unicorn Zomato tore and burnt their uniforms in Kolkata to protest against the company. The reason: Zomato is funded by Ant Financial, an affiliate company of the Chinese e-commerce giant Alibaba.

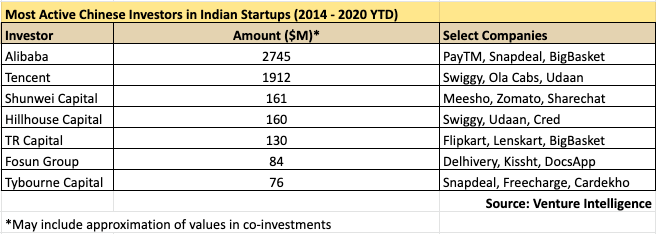

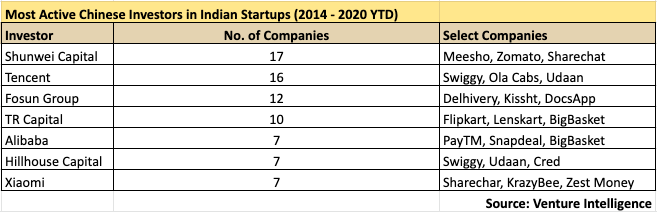

Zomato is neither the first Indian company to face a backlash for being backed by Chinese investors, nor it would be the last. After all, Chinese investors have pumped in almost USD 5.82 billion in Indian startups since 2014, according to the data collated by Chennai-based research firm, Venture Intelligence. More than half of the 25 Indian unicorn companies, including Paytm, Policybazaar, Byju’s, Swiggy, and many others, have Chinese investors on their cap table.

Despite the increasing socio-political angst for Chinese products and companies, what has really been keeping investors awake at night is the amendment in foreign direct investments (FDI) rules that India implemented in April. The Indian government made it mandatory for investors from the countries that share land-border with India, such as China, to take prior approval to invest in an Indian company. The move was evidently aimed at blocking potential takeovers of Indian companies by Chinese firms.

However, industry veterans feel just because Indian founders are getting money from China doesn’t mean they have lost control of their company.

“As far as the investors’ side of the table is concerned, the important thing to look at is, what is the degree of control that the investors actually have as opposed to simply the quantum of money invested,” said Siddarth Pai, founding partner of 3one4 Capital, a Bengaluru-based VC firm.

“Most of the Indian investors and entrepreneurs were already highly sensitive to the question of control that actually comes in with foreign funding,” he said. “The public also will start becoming cognizant of this fact.”

Investors who KrASIA spoke to, believe things are likely to normalize once some consensus is reached between the two countries.

A US-based investor, who declined to be named, believes there will be turbulence due to geopolitical issues between India and China in the short term, but in the long term, things will have to go back to normal. “A lot of it depends on how the political situation works out. I think both China and India are large economies and it’s not in anyone’s interest to escalate this,” he said.

Meanwhile, the startup and VC community in the country is preparing to absorb the impact that comes along with the lack of investment from Chinese firms.

The startups’ plight

The double whammy of tightened FDI rules for Chinese VCs and anti-China sentiments due to the recent stand-off could not have come at a worse time for startups that have been weathering the COVID-19 induced slump.

Now there are factions among Indians calling for boycotting startups that have been sourcing material from China or that are backed by Chinese funds. This is in addition to boycotting Chinese firms that operate in the country.

The more severe impact, however, is on Chinese funded Indian startups that were hoping to raise follow-on rounds this year but may not be able to do so. Since Chinese VCs need government approval to write checks and transfer money to their Indian portfolio companies, it has become difficult for them to participate in the follow-on rounds at the same time as other investors.

“Any new investors coming in will always ask the existing investors whether they will be following-on in their investments or not, because it is a vote of confidence for new investors that the old investors still believe in the company and recommit to investing additional capital at a higher valuation,” said Siddarth.

Chinese investors can’t keep waiting for approval to come to close the round since “speed is of the essence when it comes to the highest quality startups,” he said. “Most of them [startups] end up raising capital when they have close to about nine to twelve months of runway left, so the entire ecosystem is biased towards time-efficient decision making.”

That Chinese-backed products may face a similar backlash in the future as well, makes the entire proposition even less enticing. It may, thus, also become harder for these startups to raise money from new investors.

“The risk is that Chinese investors may not be able to put in additional investment,” said Anil Joshi, managing partner at Unicorn India Ventures. However, Joshi believes startups that rely on splurging money to gain market share and depend on their investors will struggle, “but the category leaders will not find it difficult to raise money.”

The FDI policy tweak, Siddarth said, is although considered as a geopolitical move in the interest of national security rather than purely economical one, it has an economic fallout. He added the economic fallout–the shortfall in investments– has to be made up by other investment sources, including domestic capital.

Cash starved Indian startups

According to investors who KrASIA spoke to, India is a capital-starved country. While the South Asian nation has plenty of early-stage investors, those who can write checks for growth and late-stage startups are far and few in between.

“The reality is that we have to understand there is just not enough domestic capital for Indian startups to grow,” said Deepak Gupta, founding partner at WEH Ventures. “The Indian capital base is growing but at a gradual rate, so it will take some time to catch up.”

“There are very few Indian investors who can lead a USD 20-30 million round,” said another Indian investor who declined to be named. “Indian startups need outside money, whether it is Japanese, Korean, Chinese, or the US. The color of that money won’t matter much.”

Siddarth believes while there have been barriers that hinder the growth of domestic capital, the government is now looking at measures to resolve the situation.

“We have seen pension funds from Australia and Canada, and sovereign funds from the Middle East coming in, but we haven’t seen India’s LIC or larger pension schemes investing into startups,” he said. “But while the government is closing one door, it is actually opening a window by establishing incentives for domestic capital to come in and fill that gap.”

According to him, the government is making the domestic capital anchored by it available for investments. There are regulations that prevent larger insurance companies and banks from investing in startups, the latter being considered risky investments by traditional financial institutions because most of the startups are unprofitable during the high growth stage.

Read this: Zomato awaits investment from Ant Financial amidst regulatory uncertainty

“Government is looking at increasing the scope within the current norms, taking cognizance of the fact that if a particular startup is not profitable as of now, it doesn’t mean it can be classified as bad investments, and that they need to look at the economic reality of that particular company,” Siddarth said.

Now that the Chinese funding may dry up, investors believe Indian companies are seeing an increasing interest from investors across the world.

“Reliance has raised over USD 15 billion, and not a single Chinese investor in that. The vacuum created by Chinese VCs will offer opportunities for other investors to grab on,” said Unicorn Ventures’ Joshi.

“Many funds from the Middle East and European countries would look at India, trying to grab a Reliance Jio kind of opportunity, which is leveraging digital play,” he added.

According to WEH Ventures’ Gupta, non-Chinese investors are already talking to some of their slightly mature portfolio companies for investments. “Even if this space is vacated to some degree, the capital will come.”

Chinese VCs won’t let others eat their cake

Over the last five to seven years, VCs from China have invested their time and money into the Indian startup ecosystem, backing many first-time entrepreneurs. While they have been aggressive in scouting deals, they are also known for being more liberal with valuations.

They did not mind paying an amount much higher than the prevailing premium in order to get a good deal, as per the industry veterans.

Apart from the money, Chinese VCs bring a lot of experience and expertise from the Chinese startup ecosystem which went through the same cycle of growth that the Indian ecosystem is currently going through.

A founder of a Bengaluru-based startup said because of the market similarity with China, entrepreneurs have a much better scope for learning from Chinese funds versus European or US funds.

“Besides their speed and valuations that they offer, the learnings from these guys is priceless,” he said.

Read this: India just banned 59 Chinese apps, including some of country’s most popular

According to Santosh Pai, Partner at Link Legal India Law Services and an expert on cross-border investments between India and China, the cost of changing the habit of Indian consumers has been largely borne by Chinese investors.

“Household names such as Swiggy, Zomato, Bigbasket, Paytm, and Byju’s, backed by Chinese investors, have gone through an extremely difficult phase of changing the consumer habits of buying and ordering things online,” he said.

Now that India has reached an inflection point where half a billion consumer base is ready to be tapped and most of the internet companies are gearing towards reaping the benefits of the hard work they did over the years, Santosh believes it is highly unlikely that Chinese investors will let others eat their cake.

Chinese investors are perceived as being pragmatic by the larger VC fraternity. It is believed that they won’t take haircuts on their existing investments, rather they would build on them. That may, however, hold true only for bigger players. Some Chinese investors that hold minority stakes in startups, according to a report by local media Economic Times, are looking for exit opportunities, sensing that follow-on investments are going to be difficult.

“We have already started working on some new Chinese investment transactions after the new FDI regulations came in,” Santosh said. “In the next two to three months, it will be evident whether the Indian government is giving approvals for such investments or not.”

So far, according to industry insiders, the government hasn’t approved any Chinese investment. Not surprisingly, funding from Chinese investors stood at around USD 263 million across 15 deals year-to-date, as per Venture Intelligence.

If the approvals come easy, things won’t change as dramatically for Chinese VCs.

The mere requirement of approval is not a problem, because Chinese investors have sufficient interest in India to comply, according to Santosh.

“But if every approval is going to take several weeks, and hinders fundraising efforts, then Chinese funds, especially the new ones, will restructure in a way that it would be difficult to call them Chinese,” he said. “Because VC investments are easiest to re-route in India.”

As such, it is difficult for one to explain a particular fund is Chinese because most of these funds are registered in offshore jurisdictions and have pooled funds from a number of limited partners (LPs) across countries. Alternatively, the Chinese funds might start telling Indian companies to incorporate holding structures outside India such as in Singapore, so that they can put in money there, said Santosh.

“Essentially, you are making the process much more complicated, but you are not addressing the cause, because the money would still come, just through a very different mechanism,” he added.