Read China Venture Roundup for key weekly takeaways about China’s tech venture and investment landscape. KrASIA keeps you updated on China’s most active investors, promising startups and the hottest verticals of the moment—bringing you closer to one of Asia’s most developed tech ecosystems.

This new series will be published every Tuesday—sign up here to get this directly sent to your inbox each week!

Editors’ Note

Overall venture capital enthusiasm declined for the week of 27th September to 4th October. Investments made were concentrated around Series B funding and strategic investments. Healthcare and enterprise services continue their hot streak by remaining in the top three industries.

On the macroeconomic front, China’s Manufacturing Purchasing Managers Index (PMI) was 51.5% in September. It is 0.5 percentage points higher than that of the previous month, indicating that the manufacturing industry is recovering. The non manufacturing business activity index in September was 55.9%, up 0.7 percentage points from the previous month, and has remained above the critical point since March.

This week’s VC trends to note

The week saw a total of 63 investments made, a significant dip from last week’s 102.

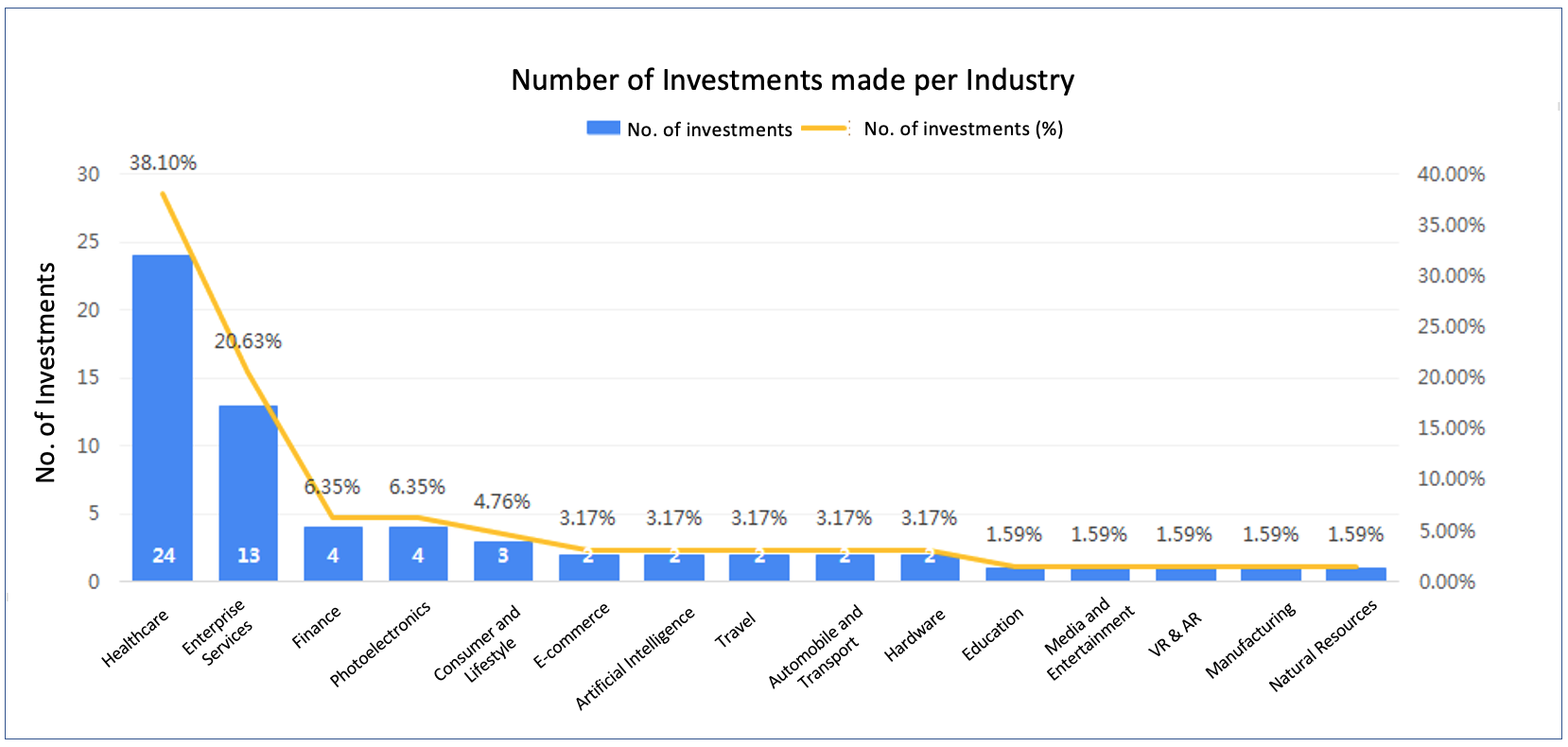

In terms of industry performance, the top 3 verticals this week are: healthcare (24 investments, accounting for 38.1%), enterprise services (13, 20.6%), finance (4, accounting for 6.3%) and photoelectronics (4, 6.3%). Healthcare and enterprise services maintain their hold on capital favour.

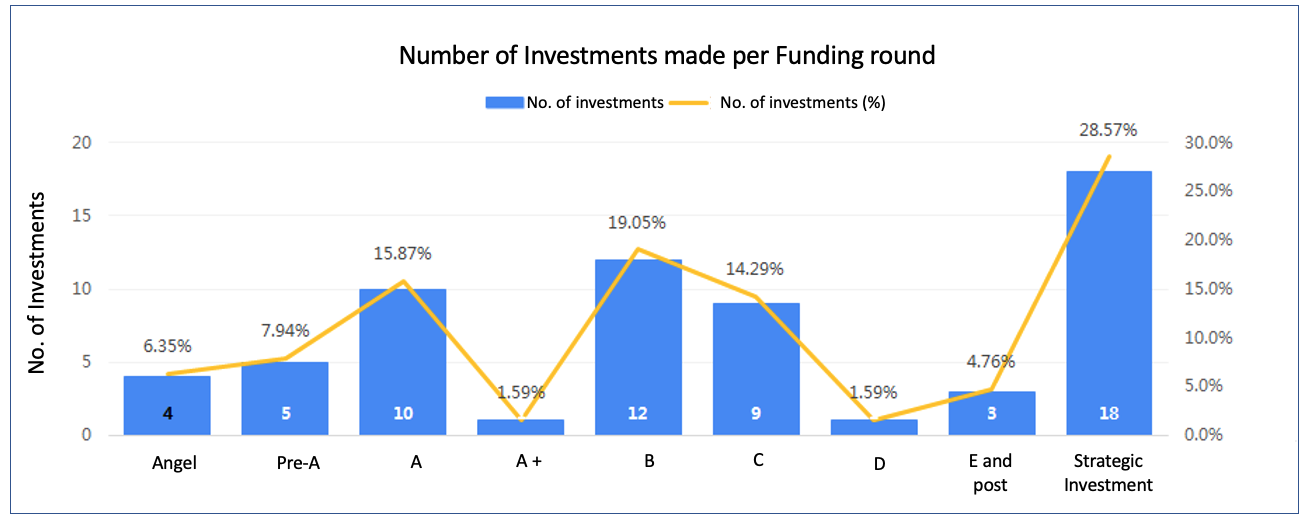

Looking at funding rounds, investments were concentrated on strategic investments (18 investments, accounting for 28.6%), followed by Series B (12, 19%), and Series A (10, 15.9%). Among them, the number of strategic investments increased slightly from the previous week, while the number of Series A investments decreased.

This week’s investment news

The number of big ticket investments (exceeding RMB 100 million) for the week was 29, down from the previous week’s 47. The top 3 high value industries are healthcare (14), enterprise services (3), while finance, automobile and transportation, and photelectronics are tied for 3rd place with 2 investments each.

Finance, in particular, performed well this week with three out of the four investments exceeded RMB 100 million.

The biggest investment made this week comes from the auto industry – the RMB 4 billion strategic investment into Xiaopeng Motors (小鹏汽车). On September 26, Xiaopeng Motors announced the exploration version of its ultra low altitude flying vehicle at the annual Beijing Auto Show. Two days later they announced its RMB 4 billion funding.

Investors include Softbank Vision Fund, Genesis Capital, Canada Pension Plan Investment Board (CPPIB), International Finance Corporation under the World Bank and CMC Capital.

New Ruipeng Pet Healthcare Group (新瑞鹏宠物医疗集团) too recently received hundreds of millions of US dollars in strategic financing. Led by Tencent, investors include German pharmaceutical company Boehringer Ingelheim, Country Garden Venture Capital, Snow Lake Capital, OrbiMed, ASPEX Management, Lake Bleu Capital and other domestic and overseas investment institutions. With this round of funding, Ruipeng Group is now valued at RMB 30 billion.

This week’s fund news

Dao Foods Venture Fund I was established on 27th September. Its LPs include Dao Food International (道夫子食品国际公司) and US-based New Crop Capital. Matrix Partners as well as several family offices and influential investors joined in. The latter includes the renowned Wayne Silby, co-founder of the USD 15 billion Calvert Impact Capital. Dao Foods Venture Fund I will focus on supporting and investing in 30 alternative protein food start-ups across the next three years.

Qingdao Blue Star Equity Investment Fund (青岛蓝色星空股权投资基金) is a joint fund established between Media Nylon and Qingdao Travel Investment Zhongjun Investment Management. The latter has been appointed as fund manager for the RMB 30.1 million fund.It mainly invests in the military-civilian integration related industries which are aligned with the national industrial strategy, have good growth prospects or demonstrate leading advantages in the field.

Jingdezhen Special Ceramic Equity Industry Investment Partnership (景德镇特种陶瓷股权产业投资合伙企业) is a joint fund between Jianfeng Electronics, Jindezhen Urban Investment Financial Holiding and Ningbo Haichuang Tongyao (宁波海创同耀投资中心). Ningbo Haichuang Tongyao Investment Center is will manage the fund’s RMB 100 million.

Zhongshan Zhonghui Guangfa Xinde Equity Investment Fund (中山中汇广发信德股权投资基金), jointly established by Edvantage Group, GF Xinde Investments and GF Qianhe, aims to raise RMB 500. Fund manager will be GF Xinde Investments. The main scope for investment includes, but is not limited to, advanced manufacturing of environmental protection equipment and new economic industries.

Zhaoying Zhucheng Industrial Upgrading Fund (招盈诸城产业升级基金) was jointly established on September 30 by China Merchants Group Capital Investment (CMC Capital) and the local government of Zhucheng, Shandong Province. With the initial RMB 600 million, CMC Capital will manage the fund, focusing on advantageous industries within Zhucheng city. The fund ultimately plans to raise RMB 2 billion by the end of 2020.

This week’s note-worthy startups

Consumer

OakiDoki (小麦欧耶); Founded 2019, received angel investment

Local oat milk startup OakiDoki received RMB 10 million of Angel investment through Vision Capital. Since its product launch in July, OakiDoki has seen steady growth, with sales doubling each month.

Oat milk sees certain demand even in the Chinese market. Well-known brand Oatly was also warmly welcomed by Chinese consumers ever since entering the Chinese market.

Enterprise Services

Easydatalink (神州云合); Founded in 2016, raised Series A

Easydatalink provides tax declaration Saas services for enterprises. It successfully raised its Series A with RMB tens of millions exclusively invested by Sequoia Capital China. Founder Zhou Qibing stated that the investment will go into sales and market development as well as to building their service system.

As the Ministry of Finance issued the notice on standardising the filing of electronic accounting documents for reimbursement in March 2020, the computerisation of finances and taxation has become an important part of enterprise information systems upgrading. Concurrently, with the gradual digital implementation of input management, output management and electronic invoicing, the demand for digital tax declaration rapidly increases. Easydatalink thus solves the many pain points in the traditional tax declaration process.

StartDT (奇点云); Founded in 2016, raised Series B

On 28th September, data center service provider StartDT announced its successful series B round, closed at RMB 120 million. This round of investment was led by Volcanics Venture and DT Capital Partners; followed by Morningside Venture Capital and Yuanyi Capital. Morningside Capital is a return investor, having previously invested in StartDT’s previous 3 rounds.

StartDT’s technology and business model lies in building data platforms and intelligent applications through big data and AI capabilities, combining industry scenarios and enterprise business. It currently serves clients in the retail industry, covering both upstream and downstream.

Shanghai Fanxi (上海泛汐); Founded in 2017; angel investment

Robotic Process Automation (RPA) company Shanghai Fanxi recently received millions of RMB in Angel investment. According to HFS Research, the global market size of RPA has increased from USD 612 million in 2016 to USD 1.714 billion in 2018, with an annual growth rate of more than 50% in the past three years. It is estimated that by 2022, the market size will reach USD 4.308 billion, and the domestic market alone will reach USD 10 billion.

Healthcare

BociMed (博志研新); Founded in 2012; raised Series B

BociMed successfully raised its Series B, gaining more than RMB 100 million of investment. The round was led by Changjiang Innovation and followed by VStone Capital and return investor Richen Capital. This round of funds will be used for the construction of a FDA approved pilot production base. This production base will be combined with the BociMed’s existing Contract Research Organisation to accelerate the R&D and industrialisation of innovative drugs and drug preparation.

BociMed is an enterprise engaged in drug R&D and clinical research. Through the establishment of their standardized service system, it provides R&D and outsourcing services including drug discovery, preclinical pharmaceutical R&D, phase I-IV clinical trials and drug registration and declaration.

At present, the company has its R&D headquarters in Shaghai, R&D centre in Nanjing and clinical subsidiary in Chegdu. Its products cover a variety of treatment fields such as tumour, cardiovascular, immune, nerve and psychiatric.

Automobile

YIAUTO (宜买车); Founded in 2015, raised Series B

Known as the national car marketplace brand, YIAUTO raised RMB tens of millions for its series B. This round was led by Sky9 Capital, followed by return investor Bluerun Ventures, GGV Capital and K2VC. Lighthouse Capital acted as the official financial advisor for this round.

YIAUTO is positioned as the national brand of new automobile supermarkets, providing one-stop car purchase services for customers all over the country. Starting from the third and fourth tier cities and aimed at being the secondary distributor,

YIAUTO has solved the three core problems of “vehicle supply, customer demand and transaction site” in automobile distribution. Relying on the support of supply chain, it provides consumers with complete categories, high cost-effective cars and well-standardized services. At present, it has 200+ self-operating stores covering 10 provinces.

This week’s policy news

- Statistics Bureau: China’s Manufacturing Purchasing Managers Index (PMI) in September was 51.5%, up 0.5%

According to the Bureau of statistics, China’s Manufacturing Purchasing Manager Index (PMI) was 51.5% in September. The 0.5% increase form August is an early indication that the manufacturing industry is recovering. In September, the non-manufacturing business activity index was 55.9%, up 0.7% from August, and has remained above the critical point since March.

- National Medical Insurance Bureau: by the end of 2021, direct settlement of outpatient expenses will be enacted across provinces

Huang Huabo, director of the fund supervision department of the State Medical Security Bureau, announced that the National Medical Insurance Bureau will further expand the pilot scope of cross provincial direct settlement of outpatient expenses. This will accelerate the formation of a nationwide, universal cross-provincial direct settlement system, operation mechanism and processes.

The aim is for the direct settlement of outpatient expenses to be enacted across all provinces by the end of 2021. Thus providing insured people with more convenient and efficient direct settlement services for remote medical treatment as well as inpatient and outpatient services.

- People’s Bank of China (PBC) and the China Banking and Insurance Regulatory Commission (CIRC) issued the notice on the establishment of a countercyclical capital buffer mechanism

People’s Bank of China and the China Banking and Insurance Regulatory Commission issued the notice on the establishment of a countercyclical capital buffer mechanism, to be implemented on 30 September. The circular specifies the accrual method, coverage and evaluation mechanism of China’s countercyclical capital buffer.

According to the current situation of systemic financial risk assessment and the needs of epidemic prevention and control, it is clear that the counter cyclical capital buffer ratio is initially set as 0, without increasing the capital management requirements of banking financial institutions. PBC and the CIRC will comprehensively consider the macroeconomic and financial situation, leverage ratio and the stability of the banking system, and regularly assess and adjust the countercyclical capital buffer requirements to prevent systemic financial risks.

- State‑owned Assets Supervision and Administration (SASAC): accelerate the divestiture of non main businesses and inefficient and ineffective assets, and further promote the removal of “zombie enterprises”

On September 29, China’s State‑owned Assets Supervision and Administration (SASAC) held a video conference to mobilize and deploy the three-year action of central enterprise reform. The meeting stressed that it is necessary to support central enterprises to promote the coordinated development of private enterprises and small and medium-sized enterprises, and to promote the concentration of state-owned capital in important industries and key fields.

It is also necessary to enhance the ability of independent innovation, increase R&D investment, and improve the collaborative innovation system, so as to make greater progress in tackling key core technologies and transforming and applying scientific research achievements. The progress of such activity will be consolidated continuously, the stripping of non main businesses and inefficient and invalid assets accelerated, and “zombie enterprises” will be clamped down.

- National Association of Financial Market Institutional Investors issued the detailed rules for the hierarchical and classified management of debt financing instruments of overseas non-financial enterprises

The National Association of Financial Market Institutional Investors issued the detailed rules for the hierarchical and classified management of debt financing instruments of overseas non-financial enterprises and the registration document form of debt financing instruments of overseas non-financial enterprises to optimize the registration and issuance management of panda ponds of non-financial enterprises.

The optimization of panda bond registration and issuance of non-financial enterprises adheres to the direction of marketization, legalization and internationalization, adheres to the concept of registration system, improves the process of panda bond registration and issuance mechanism, optimizes information disclosure specifications, improves business convenience and transparency, focuses on establishing a positive incentive mechanism for panda bond issuance, and improves the quality of inter-bank market opening and international influence.

- Ministry of Industry and Information Technology: accelerating the healthy development of lithium ion battery industry

The Ministry of industry and information technology attaches great importance to the development of lithium-ion battery. It has restated its will to actively work with relevant departments to adhere to comprehensive policies, continue to organize and implement the “standard conditions for lithium-ion battery industry”, guide the rational industrial layout and resource integration, avoid low-level repeated construction and malicious competition, and accelerate the healthy development of the mobile lithium-ion battery industry.

- Ministry of Industry and Information Technology: cultivate a number of green manufacturing suppliers to promote the rapid development of industrial solid waste comprehensive utilization industry

The special fund for sustainable manufacturing will be used to cultivate a number of green manufacturing suppliers, so as to promote the rapid development of industry utilization of industrial solid waste, strengthen cooperation with financial institutions such as China Development Bank and Agricultural Bank of China, and further implement the green credit policy for comprehensive utilization of industrial resources. Actively cooperate with relevant departments to study preferential policies for comprehensive utilization of waste rock resources such as shipping charges.

This week’s top stories

- Royole Technology wants to ‘bend the world’ – the story behind its new folding smartphone, FlexPai 2

Royole Technology recently launched its second iteration of a folding smartphone, the FlexPai 2. Despite not being a full fledged phone manufacturing brand, it has caught consumers attention by pricing its smartphone below RMB 10,000; far below existing competitors. Founder Bill Liu Zihong notes that there is a certain growth curve for phones with foldable screens, to be accepted by majority of consumers but believes the lower price can encourage quicker adoption.

A man who claims to want to ‘bend the world’, Bill Liu majored in electrical engineering at Tsinghua University and obtained his doctorate from Stanford. After leaving IBM in 2012, Bill founded Royole and launched its 0.01mm full-colour flexible display screen in 2014. This set the ground for Royale to complete 12 rounds of fundraising, and eventually begin its IPO process. 8 years later, with the popularity of flexible screens still in its infancy, Royole has entered a phase where it is necessary to apply their technology to their own products, renew their vision and tell new stories – with the exception of ZTE Devices, Royole has yet to receive orders from domestic, mainstream mobile phone manufacturers.

Royole has established six business divisions to explore more diverse business opportunities. It already has collaborations with Louis Vuitton and Airbus to land their products in the fashion and airliner industries. In addition to their to-B model, Royole has moved into the to-C realm with its RoWrite smart notebook, the FlexPai phones, VR headsets and more. Bill believes the hybrid to-B and to-C model is the best fit for Royole.

Unlike Samsung’s folding screen technology route, Ruoyu uses its trademark ultra-low temperature non silicon process integration technology (ULT-NSSP). Last year, however, Royole faced some controversy over their production numbers. While Bill has not provided specific answers, her has refuted rumours that their numbers were low by industry standards. He claims that during first phase of Ruoyu production line in 2018, they had a capacity of about 2.8 million 8-inch screens.

- Alibaba’s Dingding begins its restructuring

On the evening of September 27, 2020, Alibaba announced a new round of strategic deployment: the transformation of its enterprise app Dingding into a fully developed business unit, fully integrating with Alibaba cloud. This step is to be wholly supported by relevant units of the group to ensure complete implementation of the “Cloud- Dingding integration” strategy.

Under this premise, the original Dingding business unit, Alibaba cloud video team, Alibaba cloud Teambition, enterprise intelligence business unit, government enterprise cloud business department, digital government affairs department and the Blackbird technology team will join the new business unit, fully integrated into Alibaba cloud intelligence.

This has launched Dingding back into the spotlight.

- Between the push and the pull – how consumer brands navigate growth under changing consumer patterns

How did the GeoSkincare blow up the internet within 6 months? What about Douyin, Kuaishou and Billibilli? What is the story behind Proya cosmetics?

There is some form of a perfect synergy between the many different social media platforms. Douyin videos can be used as advertising platform and also be integrated with Tmall to drive sales volume and convert users into buyers. One can organize big-scale livestreams on Kwai and employ Billibilli to attract younger consumers. However, these platforms need to be strategically sequenced to avoid any potential clashes in the content output.

In addition, for live broadcasting and short video formats, from the perspective of a brand that hopes to create long-term influence, it is key to identify areas that can be controlled. For example, prices for live broadcasting on Tmall are well regulated, giving brands the peace of mind to work with influencers and hosts of varying popularity.

- Lingering anxieties despite the travel industry’s recent positive recovery

After being on hold for half a year, the travel industry is currently experiencing a positive rebound. According to data released by the Ministry of Culture and Tourism, during the recent National Day Holiday, 97 million domestic tourists were received in the country with revenue reaching RMB 76.6 billion, demonstrating a seven-fold recovery.

Moreover, the number of tickets issued on Ctrip increased by more than 200% over the same period last year. Its car rental platform of Ctrip has also seen a peak, with a year-on-year increase of 79%.The National Day Holiday period provides clear evidence of a warmer tourism industry.

- 2020 has welcomed a new class of LPs

Recently, a new group of LPs have been active participants in the local venture capital scene – the new generation of successful entrepreneurs and unicorns.

Even before its public listing has been completed, Bubble Mart’s founder Wang Ning has invested in 3 VC funds. Kuaishou too made its maiden investments in VCs after announcing its listing on Hong Kong’s Stock Exchange. Due to it only taking a few years for entrepreneurs to become LPs, new economic forces are on the rise, changing China’s VC trends.

This shift is made more significant in 2020 as the unprecedented difficulties VCs face in raising funds called for the entry of new LPs. However, these capital upstarts tend to believe in “one for one” and tend to invest in VCs that once supported them. That is to say, the VCs that once betted on these unicorns and entrepreneurs are the envy of others.

Note: KrASIA’s ‘China’s Venture Roundup Volume.5’ was adapted from 36Kr’s Venture Weekly series